Accounting Rate of Return

advertisement

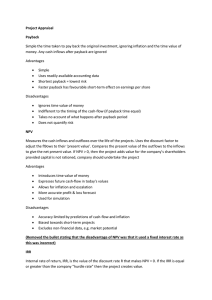

19 Capital Investment 19-1 Payback and Accounting Rate of Return: Nondiscounting Methods 2 Payback Period: the time required for a firm to recover its original investment. When the cash flows of a project are assumed to be even, the following formula can be used to compute the project’s payback period: Payback period = original investment/annual cash flow If the cash flows are uneven, the payback period is computed by adding the annual cash flows until such time as the original investment is recovered. 19-2 Payback and Accounting Rate of Return: Nondiscounting Methods 2 • The payback period provides information to managers that can be used as follows: • To help control the risks associated with the uncertainty of future cash flows. • To help minimize the impact of an investment on a firm’s liquidity problems. • To help control the risk of obsolescence. • To help control the effect of the investment on performance measures. 19-3 Payback and Accounting Rate of Return: Nondiscounting Methods 2 Accounting Rate of Return (ARR) Measures the return on a project in terms of income, as opposed to using a project’s cash flow Accounting rate of return = Average income /Original investment Where: Average income = average annual net cash flows less average depreciation Original investment (or average investment) = (I+S)/2 (I is the original investment and S is the salvage value). Assume that the investment is uniformly consumed. The major deficiency of the accounting rate of return is that it ignores the time value of money. 19-4 The Net Present Value Method 3 • Net Present value is the difference between the present value of the cash inflows and outflows associated with a project: NPV = P - 1 Where: P = the present value of the project’s future cash inflows I = the present value of the project’s cost (usually the initial outlay) NPV measures the profitability of an investment. If the NPV is positive, it measures the increase in wealth 19-5 The Net Present Value Method 3 Decision Criteria for NPV If the NPV is positive, it signals that 1) The initial investment has been recovered 2) The required rate of return has been recovered 3) A return in excess of (1) and (2) has been received Reinvestment Assumption: The NVP model assumes that all cash flows generated by a project are immediately reinvested to earn the required rate of return throughout the life of the project. 19-6 Internal Rate of Return 4 The internal rate of return (IRR) is the interest rate that sets the present value of a project’s cash inflows equal to the present value of the project’s cost. It is the interest rate that sets the project’s NPV at zero. 19-7 Internal Rate of Return 4 Decision Criteria: If the IRR>Cost of Capital, the project should be accepted. If the IRR = Cost of Capital, acceptance or rejection is equal. If the IRR < Cost of Capital, the project should be rejected. 19-8 NPV versus ITT: Mutually Exclusive Projects 5 There are two major differences between net present value and the internal rate of return: • NPV assumes cash inflows are reinvested at the required rate of return, whereas the IRR method assumes that the inflows are reinvested at the internal rate of return. • NPV measures the profitability of a project in absolute dollars, whereas the IRR methods measures it as a percentage. 19-9 Computing After-Tax Cash Flows • 6 To analyze tax effects, cash flows are usually broken into three categories: 1. The initial cash outflows needed to acquire the assets of the project 2. The cash flows produced over the life of the project (operating cash flows) 3. The cash flows from the final disposal of the project 19-10 Computing After-Tax Cash Flows 6 MACRS Depreciation The taxpayer can use either the straight-line or the modified accelerated cost recovery system (MACRS) to compute annual depreciation with a half year convention The tax laws classify most assets into the following three classes (class = allowable years for depreciation): Class 3: most small tools Class 5: cars, light trucks, computer equipment Class 7: machinery, office equipment 19-11 Capital Investment: Advanced Technology and Environmental Considerations 7 How Estimates of Operating Cash Flows Differ A company is evaluating a potential investment in a flexible manufacturing system (FMS). The choice is to continue producing with its traditional equipment, expected to last 10 years, or to switch to the new system, which is also expected to have useful life of 10 years. The company’s discount rate is 12 percent. Present value ($4,000,000 * 5.65) Investment Net Present Value $22,600,000 18,000,000 $ 4,600,000 19-12