Reporting Inventory

Chapter 19

Review:

Perpetual system

Periodic system

Inventory is an asset until it is sold, at

which time it “becomes” the expense

Cost of Goods Sold.

Here is the problem:

Beg. Invent is 10 units @ $2

Purchased 20 units @ $3

Sold 15 units.

Which 15 were sold? Which 15 are still in

inventory?

Answer:

Specific I.D. - you know which ones

were sold.

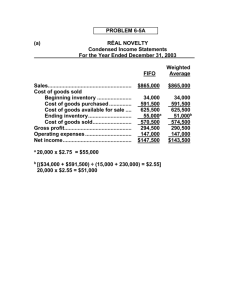

Average: (10 x $2) + (20 x $3) = $80 / 30

= $2.67 per unit cost.

FIFO: the 10 units from beg. Invent. + 5

from purchase were sold.

LIFO: the 15 from the most recent

purchases were sold.

Why so many choices?

FIFO: Gives a better Balance Sheet number

- inventory reported at most recent costs.

LIFO: Gives a better Income Statement

number for CGS - most recent costs.

Which is better, LIFO or FIFO?

Since CGS is an expense and therefore

reduces net income AND taxable income, a

company should choose the method which

results in the highest CGS.

When

prices are rising, this is LIFO.

When prices are falling, this is FIFO.

Why not use FIFO for “books”

and LIFO for the tax return?

IRS says we can’t do that! (Too bad, it

would be the “best of both worlds”.)

Inventory disclosure in financial

statements:

Must tell F/S reader what cost flow

assumption you are using.

Must report inventory at LCM. (We do this

because of the conservatism principle.)

A loss

CGS.

of inventory market value increases

Sometimes we have to estimate

inventory.

Two methods commonly used:

1.

Gross Profit method.

2. Retail method.

Gross Profit Method:

Use past data to estimate the Gross Profit

percentage.

“Work backwards” to plug in the ending

inventory. (pg. 685.)

Retail Method:

Allows retailer to take an inventory at retail

prices and then “convert” those prices to

cost.

Follow

page 686.

Cash Flow Statement

Last semester - direct method.

This chapter - indirect method. (We’ll cover

only the operating activities section & later

cover the other two sections.)

I will not lecture on this - follow the

example in your book.

The End

0

0