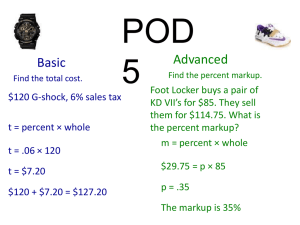

Trade Discounts, Cash Discounts, Markup, and

advertisement