Section 1: The Basic Economic Problem

1.1 Scarcity and Choice

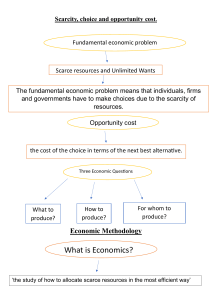

Scarcity: The fundamental economic problem arising because

resources are limited, but human wants are infinite.

Choice: Due to scarcity, individuals, firms, and governments

must make choices about how to allocate limited resources to

satisfy various needs and wants.

1.2 Factors of Production

Land: Natural resources used in the production of goods and

services.

Labour: Human effort, both physical and mental, used in the

production process.

Capital: Man-made goods used to produce other goods and

services.

Enterprise: The ability to combine the other factors of

production to produce goods and services.

1.3 Opportunity Cost

Definition: The next best alternative forgone when a decision

is made.

Example: If a student spends time studying economics instead

of working a part-time job, the opportunity cost is the

income they could have earned.

1.4 Production Possibility Curve (PPC)

Definition: A graphical representation showing the maximum

combination of goods and services that can be produced in an

economy, given its resources and technology.

Diagram:

Capital Goods

|

|

*

|

*

| *

| *

|*__________ Consumer Goods

In this diagram, the curve represents efficient production points.

Points inside the curve indicate underutilization of resources, while

points outside are unattainable with current resources.

📘 Section 2: The Allocation of Resources

2.1 Microeconomics and Macroeconomics

Microeconomics: Focuses on individual markets and the

behavior of consumers and firms.

Macroeconomics: Examines the economy as a whole,

including issues like inflation, unemployment, and national

income.

2.2 The Market System

Market Economy: An economic system where decisions

about production and consumption are driven by market

forces without government intervention.

Mixed Economy: Combines elements of market and planned

economies, with both private and public sector involvement.

2.3 Demand

Definition: The quantity of a good or service that consumers

are willing and able to purchase at different prices.

Law of Demand: As the price of a good rises, the quantity

demanded falls, ceteris paribus.

Diagram:

Price

|

| *

| *

| *

|*

|*__________ Quantity

This downward-sloping demand curve illustrates the inverse

relationship between price and quantity demanded.

2.4 Supply

Definition: The quantity of a good or service that producers

are willing and able to sell at different prices.

Law of Supply: As the price of a good rises, the quantity

supplied increases, ceteris paribus.

Diagram:

Price

|

|*

| *

| *

| *

|__________ Quantity

This upward-sloping supply curve indicates a direct relationship

between price and quantity supplied.

2.5 Market Equilibrium

Equilibrium Price: The price at which the quantity demanded

equals the quantity supplied.

Equilibrium Quantity: The quantity bought and sold at the

equilibrium price.

Diagram:

Price

|

| D

| /

| /

|/S

|/__________ Quantity

0

0