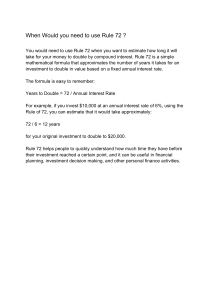

Leeds University Business School LUBS1035 Foundations of Finance Sina Erdal Lecture 2: Introduction to Valuation: The Time Value of Money Time Value of Money: Intuition Assume that today is October 4th, 2017. You can have £10,000 now… Which would you choose? What is worth more? £10,000 now or £10,000 in three years time? Or, you can have £10,000 when you graduate in 2020. Why? Too easy? Assume that today is October 4th , 2017. You can have £10,000 now… Which would you choose? What is worth more? £10,000 now or £15,000 in three years time? Or, you can have £15,000 when you graduate in 2020. Why? Overview of Lecture Future Value and Compounding Present Value and Discounting Tying it all Together The first step… Future Value and Compounding Future Value and Compounding Future value (FV) The amount an investment is worth after one or more periods. Investing for a Single Period Year 0 • You invest £100 at 10% Year 1 • Your money grows to £100 + 10% of £100 = £110 Investing for a Single Period In general: V1 V0 (1 r ) Where V1 is the value at time t = 1; r is the interest rate Some Terminology Compounding • The process of accumulating interest on an investment over time to earn more interest. Interest on Interest • Interest earned on the reinvestment of previous interest payments. Some Terminology Compound Interest • Interest earned on both the initial principal and the interest reinvested from prior periods. Simple Interest • Interest earned only on the original principal amount invested. Example (see example 4.1) Interest on Interest Suppose you locate a two-year investment opportunity that pays 10 per cent interest per year. You decide to invest £100. Required: Calculate what the total investment will be worth at the end of the two years. Calculate how much simple interest you have received. Calculate how much interest on interest you have received Calculate how much compound interest you have received. Investing for More than One Period Year 0 • Invest £100 at 10% Year 1 • £100(1.1) = £110 Year £100 invested plus £10 simple interest • £110(1.1) 2 = £121 £100 invested plus £20 (2 x £10) simple interest plus £1 interest on interest Interest on Interest Solution: Calculate what the total investment will be worth at the end of the two years. • The total investment is worth £121 (£100 x 1.1 x 1.1) Calculate how much simple interest you have received. • The simple interest is £20 (£100 x 10% x 2) Calculate how much interest on interest you have received. • The interest on interest is £1 (£100 x 10% x 10%) Calculate how much compound interest you have received. • The compound interest is £21 (£121 - £100) Investing for More than One Period Year 0 Invest £100 @10% Year 1 £100 x 1.1 = £110 Year 2 £110 x 1.1 = £121 Investing for More than One Period Year 0 Invest £100 @10% Invest £100 @10% Year 1 £100 x 1.1 = £110 £100 x 1.1 = £110 Year 2 £110 x 1.1 = £121 £100 x 1.1 x 1.1 = £121 Investing for More than One Period Year 0 Invest £100 @10% Invest £100 @10% Invest £100 @10% Year 1 £100 x 1.1 = £110 £100 x 1.1 = £110 £100 x 1.1 = £110 Year 2 £110 x 1.1 = £121 £100 x 1.1 x 1.1 = £121 £100 x 1.12 = £121 Investing for More than One Period Year 0 Invest £100 @10% Invest £100 @10% Invest £100 @10% Invest V0 @ r% Year 1 Year 2 £100 x 1.1 = £110 x 1.1 = £110 £121 £100 x 1.1 = £100 x 1.1 x 1.1 £110 = £121 £100 x 1.1 = £100 x 1.12 = £110 £121 V0 x (1 + r) = V1 V0 x (1 + r)2 = V2 FV = Vt = V0 (1+r)t Future Value: A Generalisation Vt = V 0 t (1+r) Where Vt is the value at time t; r is the interest rate Example: Suh-Pyng Ku has put €500 in a savings account at Barclays. The account earns 7 percent, compounded annually. Required: Calculate how much Ms. Ku will have at the end of three years. Calculate how much is simple interest. Calculate how much is compound interest. Example: Suh-Pyng Ku has put €500 in a savings account at Barclays. The account earns 7 percent, compounded annually. How much will Ms. Ku have at the end of three years? How much is simple interest? How much is compound interest? The answer is: Total Amount: Simple interest: Compound interest: Example: Suh-Pyng Ku has put €500 in a savings account at Barclays. The account earns 7 percent, compounded annually. How much will Ms. Ku have at the end of three years? How much is simple interest? How much is compound interest? The answer is: Total Amount: €500 1.07 1.07 1.07 = €500 (1.07)3 = €612.52 Simple interest: €500 (.07 x 3) = € 105 Compound interest: €612.52 - €500 = € 112.52 Figure 4.1 Future Value, Simple Interest and Compound Interest • Simple interest is constant - £10 each year • Compound interest increases each year because interest is compounded on itself • Compound interest can be a powerful investment tool The Power of Compounding Simple Interest r = 8 per cent Compound Interest r = 8 per cent Invest £1 for 200 Years Invest £1 for 200 Years Interest = £0.08 Value of investment at end of Value of investment at end of 200 years 200 years: FV = £1(1.08)200 £1 + (200 x £0.08) = £4,838,949.59 = £1 + £16 = £17 A Big Difference! Figure 4.2 Future Value of £1 for Different Periods and Rates • Future Values are critically dependent on the interest rate • The higher r, the higher the FV • After 10 years at 10 per cent, £1 is worth £2.59 Over a long period, the effects can be dramatic… • After 10 years at 20 per cent, £1 is worth £6.19 The Power of Interest Compound Interest r = 8 per cent Compound Interest r = 12 per cent Invest £1 for 200 Years Invest £1 for 200 Years Value of investment at end of Value of investment at end of 200 years 200 years FV = £1(1.08)200 FV = £1(1.12)200 = £4,838,950 = £6,975,968,872 A BIG Difference! Where is this? Manhattan Island In 1626, Peter Minuit allegedly bought Manhattan Island for 60 guilders’ worth of trinkets from Native Americans. It is reported that 60 guilders was worth about $24 at the prevailing exchange rate. Was this a good deal for the Native Americans? Manhattan Island If the Native Americans had sold the trinkets at a fair market value and invested the $24 at 5 percent (tax free), it would now, about 380 years later, be worth more than $2.7 billion. Today, Manhattan is undoubtedly worth more than $2.7 billion, so at a 5 percent rate of return the Native Americans got the worst of the deal. What if the interest rate was10 percent? Manhattan Island C = $24 t = 380 years r = 10% FV = $24(1 r)t = 24 1.1380 $129 quadrillion $129 quadrillion is more than all the real estate in the world is worth today. Example 4.2 Compound Interest You’ve located an investment that pays 12 per cent per year. That rate sounds good to you, so you invest €400. How much will you have in three years? How much will you have in seven years? At the end of seven years, how much interest will you have earned? How much of that interest results from compounding? Example 4.2 Compound Interest The future value of €400 at 12 per cent after three years is calculated as follows: €400 1.123 = €561.97 After seven years, you will have: €400 1.127 = €884.27 Thus, you will more than double your money over seven years. Total interest earned is €884.27 - €400 = €484.27 Simple interest is €400 x 0.12 x 7 = €48 x7 = €336 Interest from compounding = €484.27 - €336 = €148.27 Test your knowledge Calculating Future Values Assume you deposit 10,000 Swedish Kroner today in an account that pays 5% interest. How much will you have in five years? Your solution Future Value: Your solution Future Value: 10,000 x (1.05) 5 = 10,000 x 1.2763 = SKr12,763 The next step… Present Value and Discounting Remember Future Value? Future value (FV) The amount an investment is worth after one or more periods. What about Present Value? Present value (PV) The current value of future cash flows discounted at the appropriate discount rate. Present Value: The Single Period Case Year 1 • Receive £1, interest rate is 10% Year 0 • What is the Year 0 equivalent value of £1 received in Year 1? Present Value: The Single Period Case Year 1 • Receive £1, interest rate is 10% Year 0 • V0 = £1/1.1 = £0.909 Some More Terminology Present Value • The current value of future cash flows discounted at the appropriate discount rate. Discount • Calculate the present value of some future amounts. See Example 4.5 Single Period PV Suppose you need £100 to buy final year textbooks in two years time. You can earn 10 per cent on your money. How much do you have to invest today? Present Values for Multiple Periods Year 2 • Receive £100, r = 10% Year 1 • £100/1.1 = £90.91 Year 0 • £90.91/1.1 = £82.65 Investing for More than One Period Year 2 Receive £100 Receive £100 Receive £100 Receive V2 Year 1 £100/1.1 = £90.91 £100/1.1 = £90.91 £100/1.1 = £90.91 V0 = V1/(1 + r) Year 0 £90.91/1.1 = £82.65 £100/1.21 = £82.65 £100/1.12 = £82.65 V0 = V2/(1 + r)2 PV = V0 = Vt / (1+r)t Present Value: A Generalisation Vt PV V0 t (1 r ) Where Vt is the value at time t; r is the interest rate Table 4.3 Present Value Interest Factors This figure is 1/(1.1) = 0.9091 This figure is 1/(1.1)3 = 0.7513 This figure is 1/(1.1)2 = 0.8264 Test your knowledge Calculating Present Value Assume you win £10,000 on the National Lottery but it is payable in 5 years. Assuming an interest rate of 5%, what is your win worth today? Your solution Present Value: 10,000 /(1.05) 5 = 10,000 x 1/(1.05) 5 = 10,000 x 0.7835 = 7,835 We can check this figure using the present value tables Table 4.3 Present Value Interest Factors Table 4.3 Present Value Interest Factors This figure is 1/(1.05)5 = 0.7835 Figure 4.3 Present Value of £1 for Different Periods and Rates • As the length of time increases, PV falls • As the interest rate increases, PV declines • These effects are magnified over time Overview of Lecture Tying it all Together Tying it all Together PV r ) FVt t PV = FVt / r ) t FVt r ) ] t FVt (1 r ) t Tying it all Together Compounding FV = PV x (1 + r)t Discounting PV = FV / (1 + r)t Example 4.8 Evaluating Investments Your company proposes to buy an asset for £335. This investment is very safe. You would sell off the asset in three years for £400. You know you could invest the £335 elsewhere at 10 per cent with very little risk. What do you think of the proposed investment? The wrong answer! • £400 is £65 more than £335, therefore it is a good investment. • That is correct from a financial accounting perspective; £65 represents an accounting ‘profit’ • However, it is not a correct corporate finance answer • Why? • Because, it fails to take account of the time value of money • We need to convert to either present values, or future values to make a meaningful comparison Example 4.8 Evaluating Investments – Present Values This is not a good investment. Why not? Because £400 in three years time has a present value of: £400/(1.1)3 = £300.53 £300.53 is less than the cash you have now. Because the proposed investment is only worth £300.53 now, it is not as good as other alternatives we have Example 4.8 Evaluating Investments – Future Values This is not a good investment. Why not? Because you can invest the £335 elsewhere at 10 per cent. If you do, after three years it will grow to a future value of: £335 (1 r )t = £335 1.13 = £335 1.331 = £445.89 Because the proposed investment pays out only £400, it is not as good as other alternatives we have If you can invest at 5 per cent, can you now answer this question? Assume that today is October 4, 2017. You can have £10,000 now… Which would you choose? What is worth more? £10,000 in 2017 or £15,000 in 2020? £15,000/(1.05)3 = £12,957. Wait for your money. Or, you can have £15,000 when you graduate in 2020. If you can invest at 15 per cent, can you now answer this question? Assume that today is October 4, 2017. You can have £10,000 now… Which would you choose? What is worth more? £10,000 in 2017 or £15,000 in 2020? £15,000/(1.15)3 = £9,863. Take your money now. Or, you can have £15,000 when you graduate in 2020. Activities for this Lecture Reading • Chapter 2 The Time Value of Money Assignment • Class 2 Preparation Questions