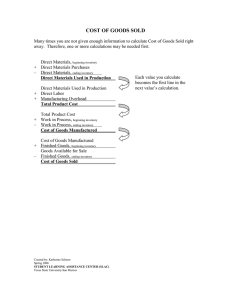

test bank managerial accounting chapter 17 process costing

advertisement