Debit and Credit Theory

Accounts

Accounts are individual items which affect financial

position.

Examples are bank, mortgage payable, land,

equipment and capital.

So far, we have grouped accounts into assets,

liabilities and owner’s equity.

The Simple Ledger

The ledger is a grouping of all of the accounts of a

business.

You may use the analogy of an account being an

individual page and the ledger as being the book

made up of those pages.

Ledgers were traditionally on cards or on loose leaf

paper, but are now almost exclusively computerized.

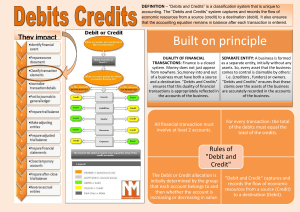

Debits and Credits

Each transaction will result in a change to at least

two accounts.

The accounts may increase (inflow) or decrease

(outflow).

Each account has two sides; a LEFT side and a

RIGHT side. We can represent this using a taccount.

ASSETS

Truck

inflows

outflows

LIABILITIES

Bank Loan

outflows

inflows

Debits and Credits

Debit is the word associated with the LEFT side and

Credit is the word associated with the RIGHT side.

Debit is abbreviated DR and Credits CR.

Assets normally carry a DR balance and Liabilities

normally have a CR balance. For now, Owner’s

Equity will normally have a CR balance but this

section has some special rules… more later!

Debits and Credits (Continued)

The dollar amount debited in a transaction must be

equaled by the dollar amount credited.

DO NOT try to memorize how accounts are affected

by transactions. Learn how to analyze each

transaction and how to apply debit and credit theory.

Debits and Credits

Also, do not think in terms of a debit being an

increase or a credit being a decrease.

0

0